Almost a fifth of households’ consumer credit originated by OFIs

7.3.2023 10:00:00 EET | Suomen Pankki | Press release

In the last quarter of 2022, households drew down EUR 80 million of unsecured consumer credit from other financial institutions (OFIs),[1] which was a little more than in the corresponding period a year earlier. The average agreed annual interest rate on new unsecured consumer credit was 9.3%. Almost a quarter of the consumer credit was drawn down from consumer credit and small-loan companies. The average interest rate on these drawdowns was 20%.

The stock of consumer credit originated by consumer credit and small-loan companies, also known as payday lenders, decreased, and the average interest rate declined in 2022.[2] At the end of December 2022, the stock of consumer granted by consumer credit and small-loan companies to Finnish households stood at EUR 154 million, with an average interest rate of 35%. Payday lenders’ stock of consumer credit has contracted significantly since 2018, when payday lenders had an estimated EUR 700 million of loan receivables from households. In September 2019, a 20%-interest rate cap on consumer credit entered into force, after which some of the companies granting small loans have discontinued either the extension of new loans or their activities altogether. The contraction of the loan stock also reflects the sale of loans off balance sheets.

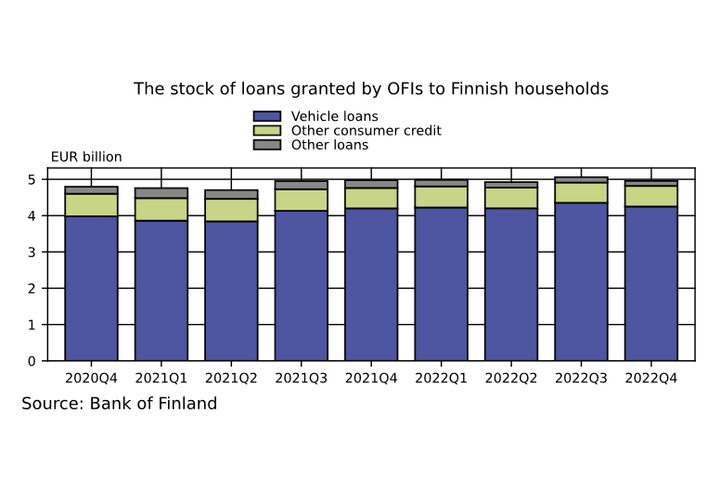

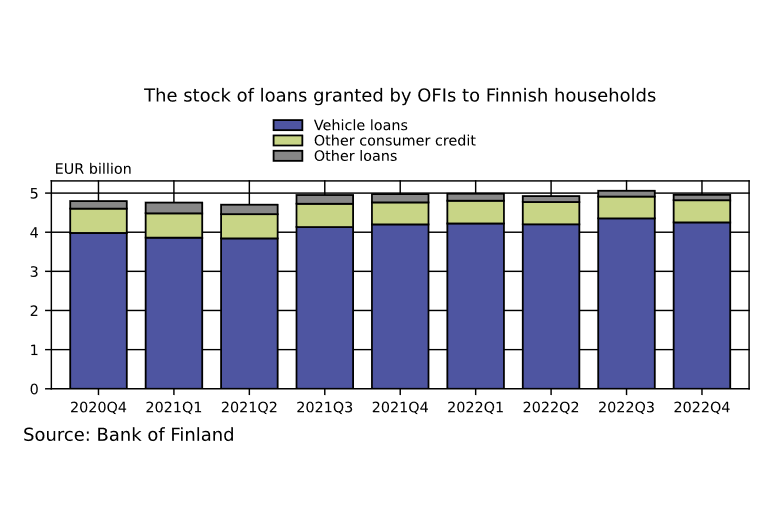

Other financial institutions originate the majority of vehicle loans

The aggregate stock of consumer credit granted by OFIs was EUR 4.9 billion at the end of 2022. Consumer credit granted by OFIs account for 19% of households’ total stock of credit (EUR 25.1 billion). The majority (68%) of households’ consumer credit has been originated by banks (credit institutions).

The majority (88%) of consumer credit originated by OFIs consisted of vehicle loans.

At present, vehicle loans constitute a more important part of OFIs’ business than before. As regards market share measured as a proportion of the loan stock, at the end of December 2022, OFIs accounted for 56% and banks for 44% of all vehicle loans (EUR 7.6 billion).

Finnish households drew down a total of EUR 1 billion of new vehicle loans from OFIs during the last quarter of 2022. The amount of vehicle loans drawn down from credit institutions in the same period was EUR 375 million. Hence, the total amount of vehicle loans drawn down in the last quarter of 2022 was EUR 1.4 billion. The agreed annual interest rate (3.4%) on new vehicle loans drawn down from OFIs in the last quarter of 2022 was lower than the interest rate on vehicle loans from credit institutions (4.7%). Likewise, the effective annual interest rate, which also includes other expenses,[3]on vehicle loans granted by OFIs was lower (5.5%) in comparison to similar loans granted by banks (6.8%).

For further information, please contact:

Tommi Salenius, tel. +358 09 183 2156, email: tommi.salenius(at)bof.fi

Markus Aaltonen, tel. +358 9 831 2395, email: markus.aaltonen(at)bof.fi

The next Other financial institutions release will be published in autumn 2023.

[1] Excl. pawnshops.

[2] At the end of 2021, the stock stood at EUR 214 million and the average interest rate was over 40%.

[3] In the OFI data collection, effective annual interest rate refers to new drawdowns, while in banking statistics, it refers to new agreements.

Images

Links

About Suomen Pankki

{kind=link}

The Bank of Finland is the national monetary authority and central bank of Finland. At the same time, it is also a part of the Eurosystem, which is responsible for monetary policy and other central bank tasks in the euro area and administers use of the world’s second largest currency – the euro.

Subscribe to releases from Suomen Pankki

Subscribe to all the latest releases from Suomen Pankki by registering your e-mail address below. You can unsubscribe at any time.

Latest releases from Suomen Pankki

Kriget i Iran driver upp inflationen och bromsar upp den ekonomiska tillväxten i euroområdet och Finland12.6.2026 11:00:00 EEST | Pressmeddelande

ECB-rådet beslutade vid sitt sammanträde i går att höja styrräntan. ”Räntehöjningen syftar till att hålla inflationsförväntningarna förankrade kring målet och förebygger en spridning av pristrycket från energi till andra priser och löner”, konstaterar Finlands Banks chefdirektör Olli Rehn.

Iranin sota nopeuttaa inflaatiota ja kolhii euroalueen ja Suomen talouskasvua12.6.2026 11:00:00 EEST | Tiedote

Euroopan keskuspankin neuvosto päätti eilen kokouksessaan nostaa ohjauskorkoa. ”Koronnostolla pyritään pitämään inflaatio-odotukset vakaasti tavoitteen tuntumassa ja ennaltaehkäisemään hintapaineiden laajenemista energiasta muihin hintoihin sekä palkkoihin”, toteaa Suomen Pankin pääjohtaja Olli Rehn.

Iran war driving up inflation and slowing growth in euro area and Finnish economies12.6.2026 11:00:00 EEST | Press release

The Governing Council of the European Central Bank (ECB) decided at its meeting yesterday to raise the key ECB interest rates. “The interest rate increase is intended to keep inflation expectations firmly around the target and to help prevent price pressures spilling over from energy to other prices and to wages,” says Governor of the Bank of Finland Olli Rehn.

Finlands ekonomi befinner sig i en vändpunkt12.6.2026 11:00:00 EEST | Pressmeddelande

Den ekonomiska tillväxten i Finland beräknas ta fart under åren framöver. Energikrisen till följd av Mellanösternkonflikten kastar dock en skugga över tillväxten och bromsar upp den ekonomiska utvecklingen och driver upp inflationen framför allt på kort sikt.

Suomen talous käännekohdassa12.6.2026 11:00:00 EEST | Tiedote

Suomen talouskasvun ennustetaan vahvistuvan vähitellen lähivuosina. Kasvua varjostaa kuitenkin Lähi-idän konfliktista johtuva energiakriisi, joka jarruttaa talouden kehitystä ja nopeuttaa inflaatiota erityisesti lyhyellä aikavälillä.

In our pressroom you can read all our latest releases, find our press contacts, images, documents and other relevant information about us.

Visit our pressroom