Housing loan stock growing at an exceptionally slow rate

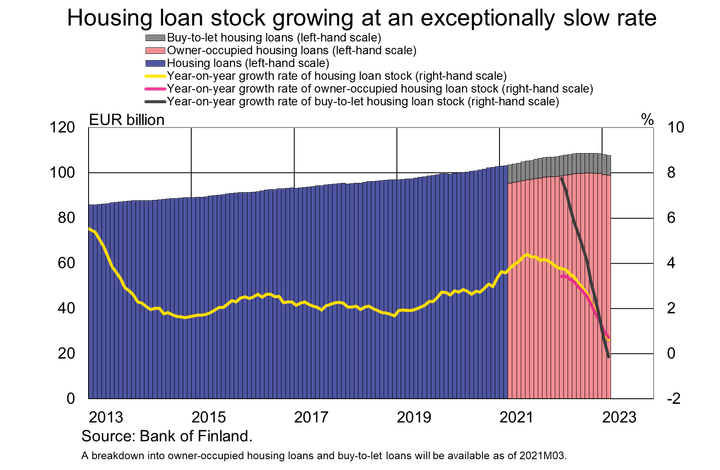

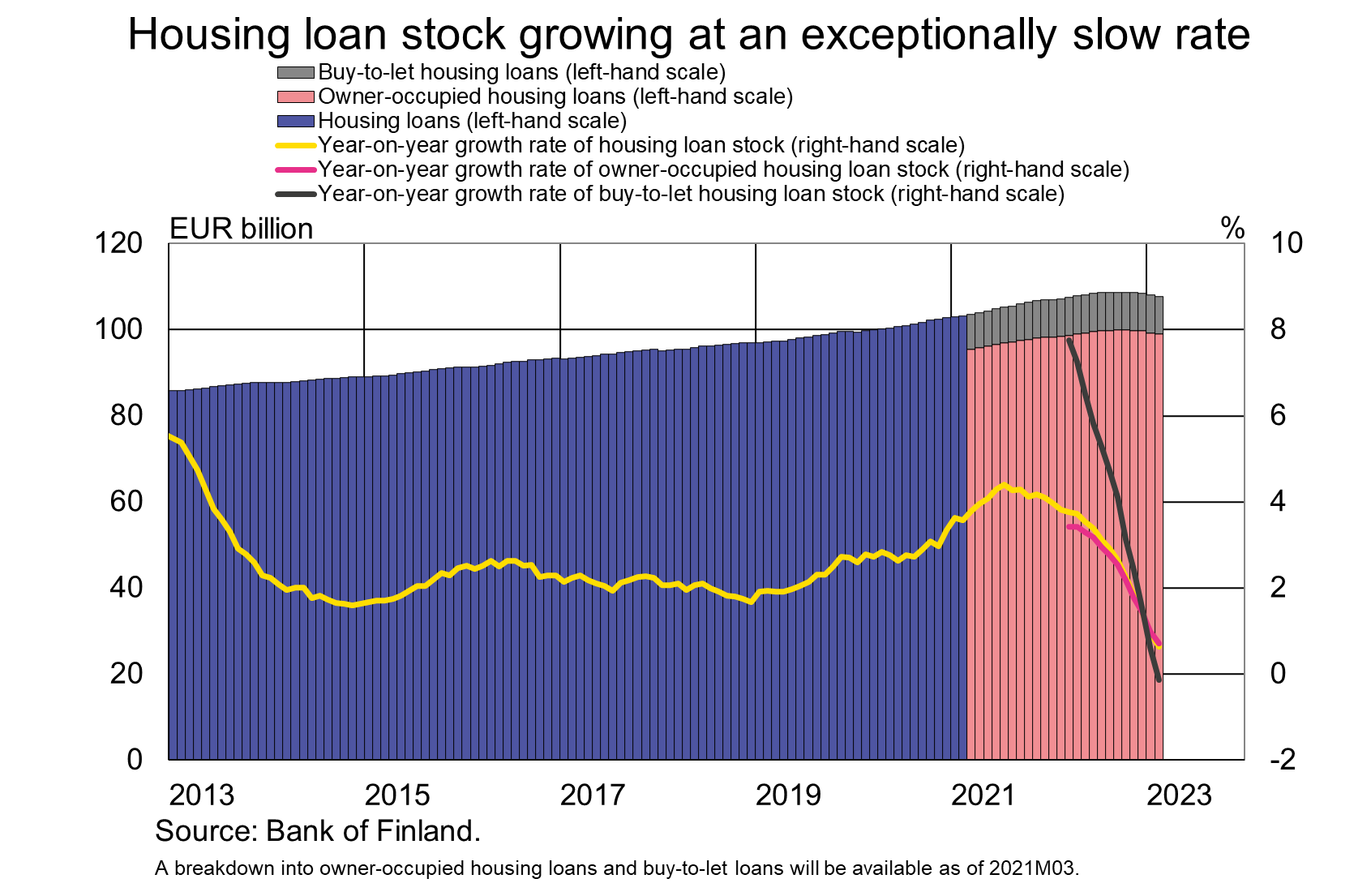

In February 2023, the year-on-year rate of growth of the stock of households’ housing loans[1] (EUR 107.9 billion) slowed down to 0.6%, having stood at 3.8% just a year earlier. Annual growth has slowed down due to decreasing drawdowns of housing loans. In February 2023, the stock of buy-to-let housing loans (EUR 8.7 billion) contracted 0.1% year-on-year, in stark contrast with a growth rate of almost 8% in March 2022. The rate of growth of the owner-occupied housing loan stock (EUR 99.1 billion) has also slowed down significantly, to 0.7%.

The drawdowns of new housing loans remained sluggish in February. In February 2023, new drawdowns of housing loans amounted to EUR 980 million. The last time housing loan drawdowns were this low in February was in 2003. In February 2023, the average interest rate on new housing loan drawdowns was 3.80%. The average interest rate on buy-to-let housing loans (4.05%) was higher than that of owner-occupied housing loans (3.78%).

In February 2023, 95% of new housing loans were linked to Euribor rates. Other reference rates are seldom used as reference rates for housing loans. As interest rates have risen, the popularity of the most common reference rate, the 12-month Euribor, has decreased in favour of shorter-term Euribor rates. In February 2023, 60% of new housing loans were linked to the 1-year Euribor, 18% to the 6-month Euribor and 17% to the 3-month Euribor. The average interest rate on new housing loans linked to the 1-year Euribor was 4.10%, in comparison to 3.59% on loans linked to the 6-month Euribor and 3.14% on loans linked to the 3-month Euribor.

According to a separate bank survey, 25% of the housing loan stock[2] was hedged against an increase in interest rates with a separate hedging product. In addition, 2.5% of the housing loan stock[3] consisted of fixed-interest rate loans. Interest rate hedges dampen the rise of the average interest rate on the housing loan stock. At the end of February 2023, the average interest on the housing loan stock was 2.38%.

Loans

At the end of February 2023, Finnish households’ loan stock comprised EUR 16.9 billion in consumer credit and EUR 18.2 billion in other loans.

Drawdowns of new loans[4] by Finnish non-financial corporations in February totalled EUR 1.4 billion, whereof loans to housing corporations amounted to EUR 390 million. The average interest rate on new corporate loan drawdowns declined from January, to 4.21%. At the end of February, the stock of loans granted to Finnish non-financial corporations stood at EUR 104.7 billion, whereof loans to housing corporations accounted for EUR 42.6 billion.

Deposits

At the end of February 2023, the stock of Finnish households’ deposits totalled EUR 110.2 billion, and the average interest rate on these deposits was 0.35%. Overnight deposits accounted for EUR 99.4 billion and deposits with agreed maturity for EUR 5.2 billion of the total deposit stock. In February, Finnish households made EUR 970 million of new agreements on deposits with an agreed maturity, at an average interest rate of 2.20%.

For further information, please contact:

Markus Aaltonen, tel. +358 9 831 2395, email: markus.aaltonen(at)bof.fi,

Ville Tolkki, tel. +358 9 183 2420, email: ville.tolkki(at)bof.fi.

The next news release on money and banking statistics will be published at 10:00 on 3 May 2023.

Related statistical data and ‑graphs are also available on the Bank of Finland website at https://www.suomenpankki.fi/en/statistics2/.

[1] Some banks recorded changes in the market value of interest rate hedges in the balance sheet item for which an interest rate hedge agreement had been signed between the bank and the customer. As interest rates rose, the revaluation adjustments recognised in the housing loan stock reduced the size of these banks’ housing loan portfolios. Due to a change in reporting practices, in December 2022, these items were no longer reported in the balance-sheet item covered by the interest rate hedge agreement. In the most recent publication, the change has been implemented in the reporting history since 2022M03. The change increased the housing loan stock in March–November 2022.

[2] At the end of June 2022.

[3] At the end of June 2022.

[4] Excl. overdrafts and credit card credit.

Images

Links

About Suomen Pankki

{kind=link}

The Bank of Finland is the national monetary authority and central bank of Finland. At the same time, it is also a part of the Eurosystem, which is responsible for monetary policy and other central bank tasks in the euro area and administers use of the world’s second largest currency – the euro.

Subscribe to releases from Suomen Pankki

Subscribe to all the latest releases from Suomen Pankki by registering your e-mail address below. You can unsubscribe at any time.

Latest releases from Suomen Pankki

En inhemsk lösning för omedelbara betalningar skulle öka funktionssäkerheten och konsumenternas valfrihet8.5.2025 11:30:00 EEST | Pressmeddelande

Finländarna måste ha tillgång till förmånliga, mångsidiga och tillförlitliga betalningssätt som fungerar säkert också under exceptionella omständigheter. En lösning för omedelbara betalningar som baserar sig på kontoöverföringar i real tid skulle öka vår förmåga att hantera systemen för betalning och erbjuda konsumenterna ett välkommet alternativ.

Kotimainen pikamaksamisen ratkaisu lisäisi toimintavarmuutta ja kuluttajien valinnanvapautta8.5.2025 11:30:00 EEST | Tiedote

Suomalaisilla tulee olla käytössään edullisia, monipuolisia ja luotettavia maksutapoja, jotka toimivat turvallisesti myös poikkeustilanteissa. Reaaliaikaisiin tilisiirtoihin perustuva pikamaksuratkaisu lisäisi kykyämme hallita maksamisessa käytettyjä järjestelmiä ja tarjoaisi kuluttajille tervetulleen vaihtoehdon.

A Finnish instant payment solution would improve resilience and consumer choice8.5.2025 11:30:00 EEST | Press release

People must have access in Finland to inexpensive, versatile and reliable methods of payment and these must function securely even in exceptional situations. An instant payment solution based on real-time credit transfers would enhance our ability to govern the systems used in making payments and would offer consumers greater choice.

Inlåningen från hushållen ökar8.5.2025 10:00:00 EEST | Pressmeddelande

Vid utgången av mars 2025 var inlåningen från de finländska hushållen (112,1 miljarder euro) 3 miljarder euro större än vid motsvarande tid för ett år sedan. Inlåningen har senast varit större 2022. I juli 2022 var inlåningen den största genom tiderna, dvs. nära 114 miljarder euro. Vid utgången av mars 2025 var 68,4 miljarder euro av inlåningen från hushållen inlåning över natten[1], 14,9 miljarder euro tidsbunden inlåning och 28,8 miljarder euro placeringsdepositioner[2].

Kotitalouksien talletuskanta kasvussa8.5.2025 10:00:00 EEST | Tiedote

Maaliskuun 2025 lopussa suomalaisten kotitalouksien talletuskanta (112,1 mrd. euroa) oli 3 mrd. euroa suurempi kuin vuosi sitten vastaavana aikana. Talletuskanta oli viimeksi suurempi vuonna 2022. Vuoden 2022 heinäkuussa se oli kaikkien aikojen suurin eli lähes 114 mrd. euroa. Maaliskuun 2025 lopussa kotitalouksien talletuksista 68,4 mrd. euroa oli yön yli -talletuksia[1], 14,9 mrd. euroa määräaikaistalletuksia ja 28,8 mrd. euroa sijoitustalletuksia[2].

In our pressroom you can read all our latest releases, find our press contacts, images, documents and other relevant information about us.

Visit our pressroom