Stock of housing corporations’ loans grew in April 2025

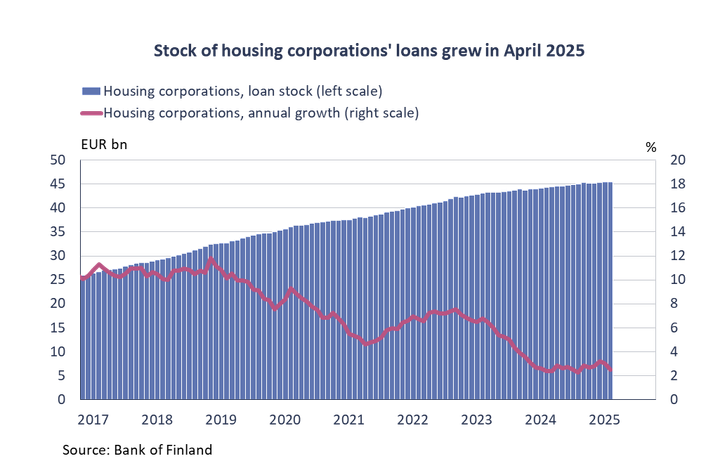

At the end of April 2025, housing corporations’[1] loan stock stood at EUR 45.4 billion, and the average interest rate on the stock (3.36%) was 1.12 percentage points lower than at the same time a year earlier. Overall, the growth of housing corporations’ loan stock has continued through the period of higher interest rates, although the stock of loans granted to private domestic limited-liability apartment house companies (housing companies), which constitutes over half of housing corporations’ loan stock, has recently contracted.[2] At the end of April, the year-on-year rate of growth of the housing corporation loan stock was 2.5%, whereas, for example, the household loan stock contracted by -0.2 and the NFC loan stock[3] contracted by -1.8%. Approximately half of the housing corporation loan stock, EUR 22.4 billion[4], was payable by households.

In April 2025, housing corporations drew down new loans in the total amount of EUR 560 million, which is 17.4% less than in the same period a year earlier. Meanwhile, the average interest rate on these new loan drawdowns was 3.15% ‒ lower than the interest rate on NFC loans (excluding housing corporations, 4.03%) or household loans (3.59%). In contrast, the average interest rate on new housing loans drawn by households was lower (2.84%) than that on housing corporations’ loans.

After the reversal of rising interest rates, housing corporations have continued to renegotiate their existing loans actively. Renegotiations of housing corporation loans began to increase in mid-2022 when interest rates started to rise. In the early part of the year (January–April) 2025, housing corporations renegotiated loans worth EUR 2.0 billion, which was 18.1% more than in the same period a year earlier. Before interest rates began to rise, in early 2022 (January-April), the amount of renegotiated loans was significantly lower, at EUR 1.2 billion.

Loans

Drawdowns of new housing loans by Finnish households in April 2025 amounted to EUR 1.3 billion, which is EUR 150 million more than in the same period a year earlier. Buy-to-let mortgage loans accounted for EUR 120 million of the new housing loan drawdowns. The average interest rate on new housing loans declined from March, to stand at 2.84% in April. At the end of March 2025, the housing loan stock totalled EUR 105.6 billion, and its year-on-year growth amounted to -0.3%. Buy-to-let mortgages accounted for EUR 8.9 billion of the housing loan stock. At the end of April, Finnish households’ loan stock comprised EUR 17.5 billion in consumer credit and EUR 17.6 billion in other loans.

Finnish non-financial corporations drew down EUR 2.4 billion in new loans[5] in April. The average interest rate on new corporate-loan drawdowns declined from March, to 3.83%. At the end of April, the stock of loans granted to Finnish non-financial corporations stood at EUR 107.0 billion.

Deposits

At the end of April 2025, Finnish households’ aggregate deposit stock totalled EUR 113.2 billion, and the average interest rate on these deposits was 1.00%. Overnight deposits accounted for EUR 68.8 billion, and deposits with an agreed maturity accounted for EUR 15.3 billion of the total deposit stock. In April, Finnish households made new deposit agreements with an agreed maturity in the amount of EUR 1.8 billion, at an average interest rate of 2.56%.

For further information, please contact:

- Ville Tolkki, tel. +358 9 183 2420, email: ville.tolkki(at)bof.fi,

- Markus Aaltonen, tel. +358 9 183 2395, email: markus.aaltonen(at)bof.fi.

The next news release on money and banking statistics will be published at 10:00 on 1 July 2025.

[1] Housing corporations include all units of institutional forms of housing. Housing companies (private domestic limited-liability apartment house companies) account for approximately 54% of the housing corporation loan stock. The remainder consists primarily of loans held by other public housing corporations and other private domestic housing corporations. Other housing corporations (than limited-liability apartment house companies) include private rental apartment groups, real estate consortia, public (mainly municipal) rental apartment companies and entities, such as apartment lessors, designated as non-profits by the Housing Finance and Development Centre of Finland, ARA. Statistics Finland is responsible for the sectoral classification.

[2] Housing corporation loans (in Finnish).

[3] Non-financial corporations, excluding housing corporations.

[4] Data on housing company loans are from end-2024 National Financial Accounts published by Statistics Finland.

[5] Excl. overdrafts and credit card credit.

Links

Bank of Finland

The Bank of Finland is the national monetary authority and central bank of Finland. At the same time, it is also a part of the Eurosystem, which is responsible for monetary policy and other central bank tasks in the euro area and administers use of the world’s second largest currency – the euro.

Alternative languages

Subscribe to releases from Suomen Pankki

Subscribe to all the latest releases from Suomen Pankki by registering your e-mail address below. You can unsubscribe at any time.

Latest releases from Suomen Pankki

Det är inte läge att skjuta upp lösningarna för Finlands offentliga finanser19.12.2025 11:00:00 EET | Pressmeddelande

Finlands offentliga finanser befinner sig alltjämt långt från balans. För att vända skuldsättningsutvecklingen krävs en betydande konsolidering av de offentliga finanserna och investeringar i tillväxt. Höjningen av de nödvändiga försvarsutgifterna försvårar den offentligfinansiella konsolideringen. Inflationen i euroområdet ligger på målet och ekonomin har vuxit något snabbare än förutsett.

Suomen julkisen talouden ratkaisuja ei kannata lykätä19.12.2025 11:00:00 EET | Tiedote

Suomen julkinen talous on edelleen kaukana tasapainosta. Velkaantumiskehityksen kääntäminen vaatii merkittävää julkisen talouden sopeuttamista ja investointeja kasvuun. Välttämättömien puolustusmenojen kasvattaminen vaikeuttaa tasapainottamista. Euroalueella inflaatio on tavoitteessa ja talous on kasvanut hieman ennustettua paremmin.

Finland’s decisions on public finances should not be postponed19.12.2025 11:00:00 EET | Press release

Finland’s public finances are still far from being in balance. Reversing the rise in public debt will require considerable fiscal consolidation and investments in growth. An expansion of essential defence spending will hamper the fiscal adjustment process. Inflation in the euro area is at target, and growth in the euro area economy has been slightly higher than forecast.

Återhämtningen i Finlands ekonomi går sakta framåt19.12.2025 11:00:00 EET | Pressmeddelande

Finlands ekonomi lämnar snart perioden med svag tillväxt bakom sig, men ingen kraftig tillväxt väntas under åren framöver. Inflationen är fortsatt måttfull och sysselsättningen stiger gradvis. Den stramare handelspolitiken och globala politiska osäkerheter samt eventuella åtgärder för konsolidering av de offentliga finanserna kastar en skugga över tillväxtutsikterna för ekonomin i Finland. De offentliga finanserna uppvisar alltjämt ett djupt underskott.

Suomen talouden elpyminen etenee maltillisesti19.12.2025 11:00:00 EET | Tiedote

Suomen talouden hitaan kasvun jakso on jäämässä taakse, mutta voimakasta kasvua ei lähivuosina ole odotettavissa. Inflaatio pysyy maltillisena ja työllisyys kohenee vähitellen. Talouden kasvunäkymiä varjostavat kauppapolitiikan kiristyminen ja kansainvälisen politiikan epävarmuudet sekä mahdolliset julkisen talouden sopeutustoimet. Julkinen talous säilyy syvästi alijäämäisenä.

In our pressroom you can read all our latest releases, find our press contacts, images, documents and other relevant information about us.

Visit our pressroom