A high amount of student loans drawn down at record-low rates in August 2020

30.9.2020 13:00:00 EEST | Suomen Pankki | Press release

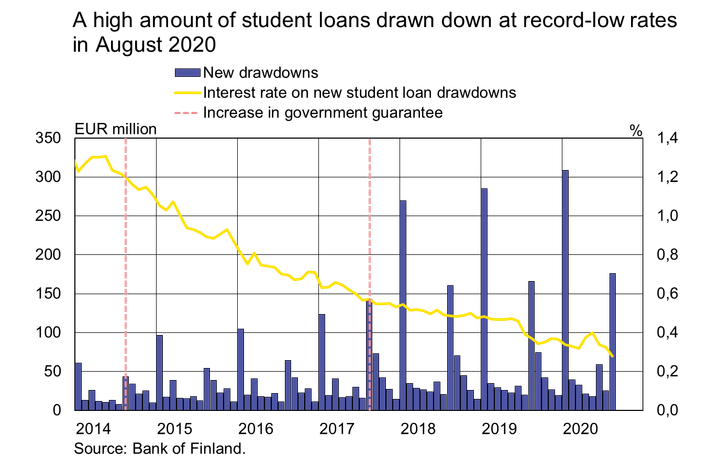

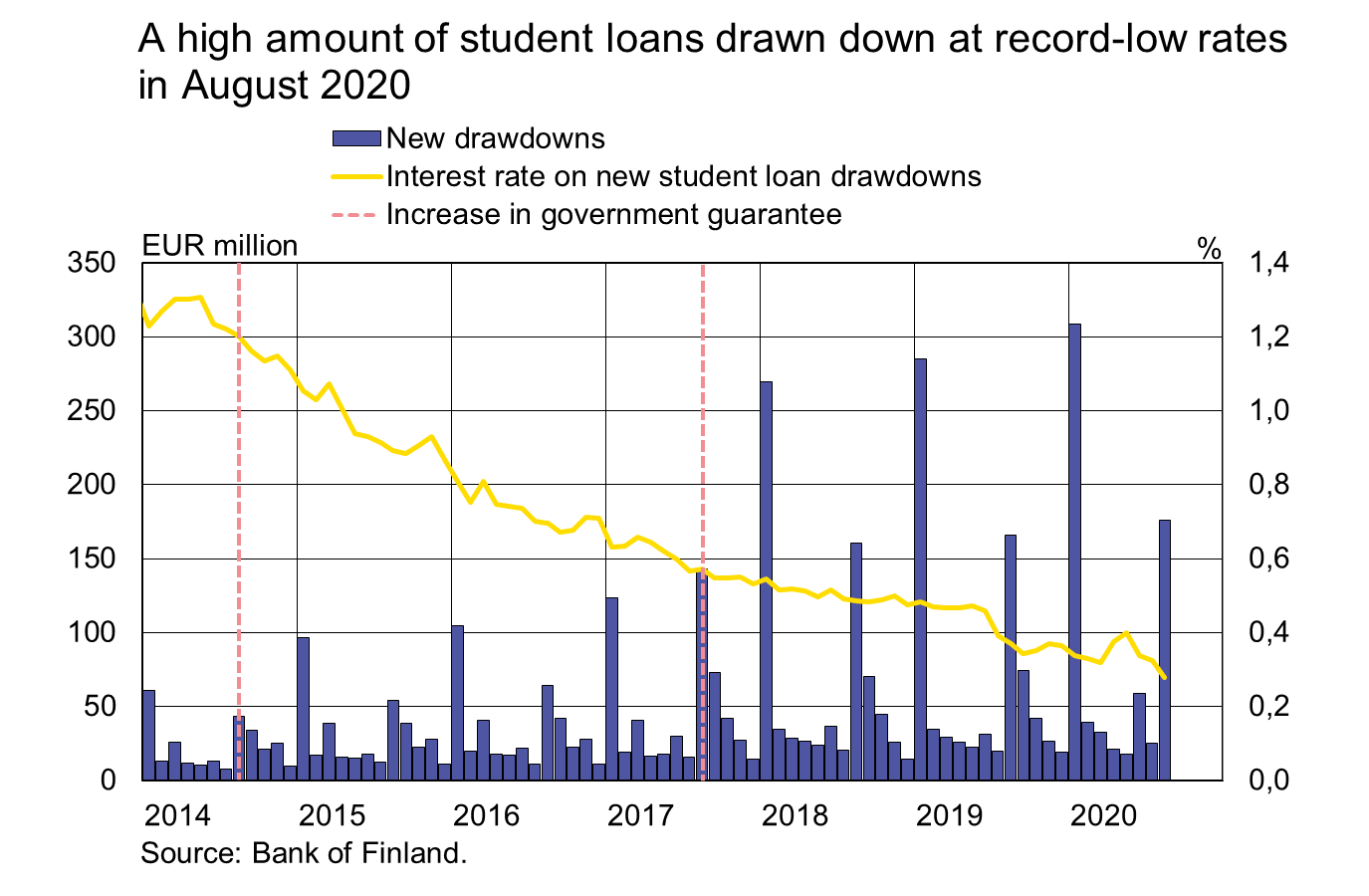

Drawdowns of student loans in August 2020 [1] totalled EUR 176 million, an increase of 6% on August a year earlier. The average interest rate on student loan drawdowns was record low in August, at 0.28%. Thanks to government guarantees, student loans pose a low risk for banks, which is reflected in the low margins on these loans.

The impact of the coronavirus crisis was particularly evident in drawdowns of student loans in June 2020: the total amount taken out was EUR 59 million, almost twice the amount compared with June a year earlier. One of the factors explaining this increase could be that there have been fewer summer jobs available during the coronavirus crisis. In addition to the greater popularity on student financial aid for the summer, many students may also have taken out their student loan for the academic year 2019–2020 as late as June this year. This was also the first time when most of the summer aid recipients could take out their student loan instalment for the autumn term already in June, which contributed to reducing the amounts drawn down in August more than in previous years. In summer 2020, student loan drawdowns were 20% higher than in the corresponding period a year earlier.

Fuelled by the high amount of drawdowns in the summer, the stock of student loans grew to EUR 4.5 bn in August 2020. The annual growth rate of the student loan stock was still brisk in August (16.1%), even though it has moderated over the past two years. Since the student financial aid reform of 2017, the student loan stock has grown by EUR 2 bn. This growth stems not only from larger loans granted as a result of the reform, but also from a higher number of borrowers, which in turn partly reflects the low level of interest rates.

Despite the brisk growth in the student loan stock, the stock of claims on government guarantees [2] contracted slightly in 2019. The repayment of student loans usually begins after the completion of studies, and the interest is capitalised as long as a student receives financial aid. Hence, any problems with loan repayment may be reflected in the stock of claims on government guarantees with a delay.

Loans

Households’ drawdowns of new housing loans in August 2020 amounted to EUR 1.7 bn, the same as in August a year earlier. At the end of August 2020, the stock of euro-denominated housing loans totalled EUR 102.1 bn and the annual growth rate of the stock was 2.7%. Household credit at end-August comprised EUR 16.8 bn in consumer credit and EUR 18.2 bn in other loans.

Drawdowns of new loans by non-financial corporations (excl. overdrafts and credit card credit) in August amounted to EUR 1.5 bn. The average interest rate on new corporate loan drawdowns declined from July, to 1.77%. The stock of euro-denominated corporate loans at end-August totalled EUR 97.4 bn, of which loans to housing corporations accounted for EUR 36.7 bn.

Deposits

The stock of Finnish households’ deposits at end-August 2020 amounted to EUR 101.4 bn and the average interest rate on the deposits was 0.07%. Overnight deposits accounted for EUR 88.8 bn and deposits with an agreed maturity for EUR 4.3 bn of the deposit stock. In August, households concluded EUR 450 million of new agreements on deposits with an agreed maturity, at an average interest rate of 0.07%.

For further information, please contact:

Markus Aaltonen, tel. +358 9 183 2395, email: markus.aaltonen(at)bof.fi

Olli Tuomikoski, tel. +358 9 183 2146, email: olli.tuomikoski(at)bof.fi

The next news release will be published at 1 pm on 30 October 2020.

Images

Links

About Suomen Pankki

{kind=link}

The Bank of Finland is the national monetary authority and central bank of Finland. At the same time, it is also a part of the Eurosystem, which is responsible for monetary policy and other central bank tasks in the euro area and administers use of the world’s second largest currency – the euro.

Subscribe to releases from Suomen Pankki

Subscribe to all the latest releases from Suomen Pankki by registering your e-mail address below. You can unsubscribe at any time.

Latest releases from Suomen Pankki

Riksdagens bankfullmäktige reser till USA4.5.2026 11:15:00 EEST | Pressmeddelande

Bankfullmäktige reser till Washington D.C. och New York den 3–8 maj 2026. Under resan träffar bankfullmäktige den högsta ledningen för amerikanska centralbanken Federal Reserve och dess regionala bank i New York samt för Internationella valutafonden (IMF). Under dessa besök informerar sig bankfullmäktige om bland annat framtidsutsikterna för den amerikanska ekonomin och den globala ekonomin, USA:s penning- och finanspolitik samt den senaste utvecklingen inom den finansiella sektorn och det internationella finansiella systemet.

Eduskunnan pankkivaltuusto matkustaa Yhdysvaltoihin4.5.2026 11:15:00 EEST | Tiedote

Pankkivaltuusto matkustaa Washington D.C:hen ja New Yorkiin 3.–8.5.2026. Matkan aikana pankkivaltuusto tapaa Yhdysvaltain keskuspankkijärjestelmän ja sen New Yorkin aluepankin sekä Kansainvälisen valuuttarahaston (IMF) ylintä johtoa. Pankkivaltuusto perehtyy näissä tapaamisissa muun muassa Yhdysvaltain ja globaalin talouden näkymiin, Yhdysvaltain raha- ja finanssipolitiikkaan sekä rahoitussektorin ja kansainvälisen rahoitusjärjestelmän viimeaikaiseen kehitykseen.

Parliamentary Supervisory Council to visit the United States4.5.2026 11:15:00 EEST | Press release

The Parliamentary Supervisory Council will visit Washington D.C. and New York on 3–8 May 2026. During the visit, the Council will meet with senior management of the Federal Reserve System (Fed), the Federal Reserve Bank of New York and the International Monetary Fund (IMF). In these meetings, the Council will review, among other things, the outlook for the US and global economies, US monetary and fiscal policy, and recent trends in the financial sector and the international financial system.

Eurosystemets penningpolitiska beslut30.4.2026 15:24:43 EEST | Beslut

ECB-rådet beslutar om penningpolitiken i euroområdet. ECB-rådet beslutade idag att hålla de tre styrräntorna oförändrade.

EKP:n rahapoliittisia päätöksiä30.4.2026 15:24:43 EEST | Päätös

EKP:n neuvosto päättää euroalueen rahapolitiikasta. EKP:n neuvosto päätti tänään pitää EKP:n kolme ohjauskorkoa ennallaan.

In our pressroom you can read all our latest releases, find our press contacts, images, documents and other relevant information about us.

Visit our pressroom