New drawdowns of investment property loans decreased more than those of owner-occupied housing loans

31.5.2022 10:00:00 EEST | Suomen Pankki | Press release

In April 2022, households’ drawdowns of new loans for investment purposes (buy-to-let mortgages) totalled EUR 128 bn, a decline of 26% from April last year. These drawdowns also declined in March, by one quarter from March a year earlier. Drawdowns of owner-occupied residential mortgages totalled EUR 1.6 bn in April, down 10% from April 2021.

The interest rates on new housing loans rose further in April 2022; the interest on investment property loans to 1.07% and the interest on owner-occupied residential mortgages to 0.92%. In April, the most common reference rate for housing loans – the 12-month Euribor – turned positive for the first time in many years. It was used in April in 90% of new investment property loans and in 87% of new owner-occupied housing loans.

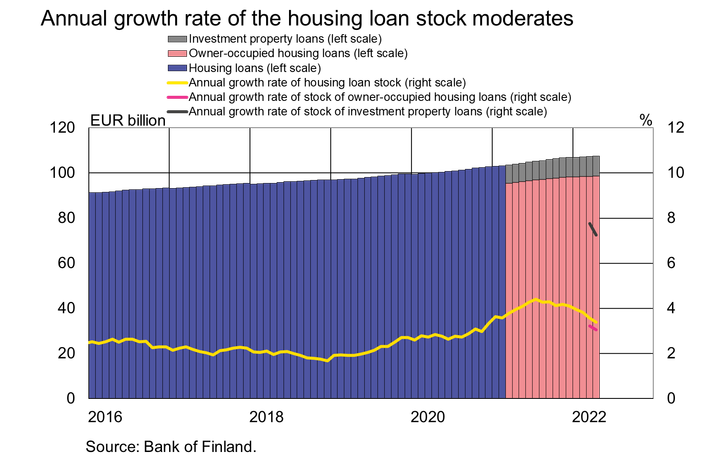

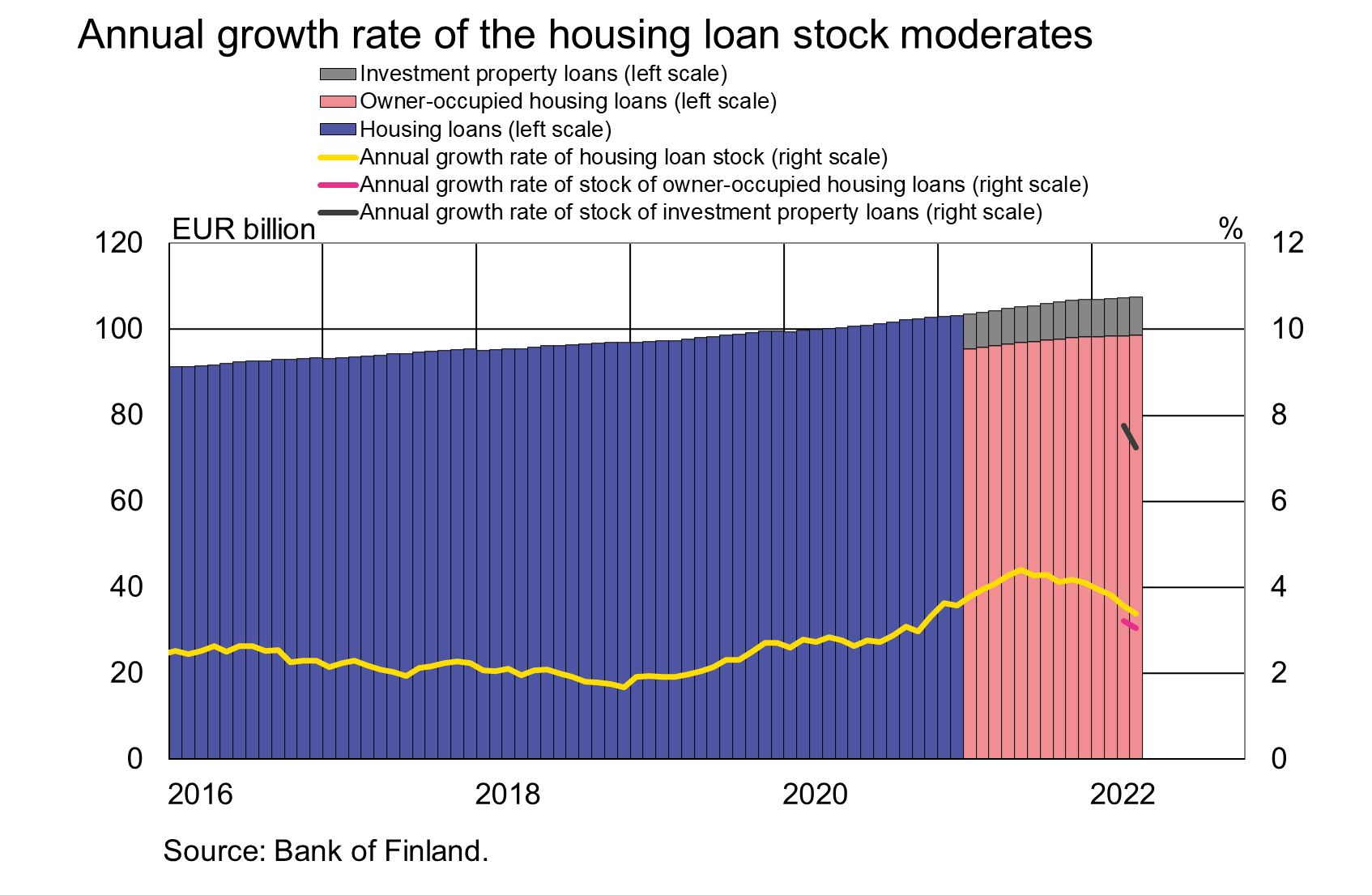

As a result of the lower amount of drawdowns, the annual growth rate of the stock of household’s investment property loans (EUR 8.8 bn) moderated by 0.5 percentage point from March, to 7.3% in April 2022. The growth rate was still considerably faster than that of the stock of owner-occupied housing loans. The growth rate (3.1%) of the stock of owner-occupied housing loans (EUR 98.7 bn) also moderated in April, but not to the same extent.

Investment property loans are typically smaller and have a longer repayment period than owner-occupied residential mortgages. In April, the average maturity of investment property loans was 18 years 6 months, as compared to 21 years 10 months for owner-occupied housing loans. In April, loans with long repayment periods, i.e. maturities of over 30 years, accounted for a record high share (12%) of new housing loans. Almost all of these loans were owner-occupied residential mortgages.

Loans

At the end of April 2022, out of all loans to Finnish households, consumer credit accounted for EUR 16.8 bn and other loans for EUR 18.2 bn.

Drawdowns of new loans[1] by Finnish non-financial corporations in April 2022 totalled EUR 2.0 bn, of which EUR 410 million were loans to housing corporations. The average interest rate on new corporate loan drawdowns rose from March, to 1.8%. At the end of April, the stock of loans to Finnish non-financial corporations stood at EUR 100.5 bn, of which loans to housing corporations accounted for EUR 40.4 bn.

Deposits

At the end of April 2022, the stock of Finnish households’ deposits stood at EUR 112.4 bn, and the average interest rate on the deposits was 0.03%. Overnight deposits accounted for EUR 103.4 bn and deposits with agreed maturity for EUR 2.1 bn of the deposit stock. In April, households concluded EUR 40 million of new agreements on deposits with agreed maturity, at an average interest rate of 0.36%.

For further information, please contact:

Markus Aaltonen, tel. +358 9 183 2395, email: markus.aaltonen(at)bof.fi

Ville Tolkki, tel. +358 9 183 2420, email: ville.tolkki(at)bof.fi.

The next news release on money and banking statistics will be published at 10 a.m. on 1 July 2022.

Related statistical data and graphs are also available on the Bank of Finland website at https://www.suomenpankki.fi/en/Statistics/mfi-balance-sheet/.

[1] Excl. overdrafts and credit card credit.

Images

Links

About Suomen Pankki

{kind=link}

The Bank of Finland is the national monetary authority and central bank of Finland. At the same time, it is also a part of the Eurosystem, which is responsible for monetary policy and other central bank tasks in the euro area and administers use of the world’s second largest currency – the euro.

Subscribe to releases from Suomen Pankki

Subscribe to all the latest releases from Suomen Pankki by registering your e-mail address below. You can unsubscribe at any time.

Latest releases from Suomen Pankki

Exporten stöder den ekonomiska tillväxten i Kina i år5.5.2026 16:00:00 EEST | Pressmeddelande

Enligt den officiella statistiken har den årliga tillväxttakten i den kinesiska ekonomin varit 5 % i fjol och under första kvartalet i år. Tillväxten har kraftigt vilat på exporten, då utvecklingen av den inhemska efterfrågan och investeringarna har varit dämpad.

Vienti tukee Kiinan talouden kasvua tänä vuonna5.5.2026 16:00:00 EEST | Tiedote

Kiinan talous kasvoi viime vuonna sekä tämän vuoden ensimmäisellä neljänneksellä virallisten tilastojen mukaan 5 % vuoden takaa. Kasvu on nojannut vahvasti vientiin, kun kotimainen kulutus sekä investoinnit ovat kehittyneet vaimeasti.

Exports support China’s economic growth this year5.5.2026 16:00:00 EEST | Press release

China’s official figures show the economy grew at an annual rate of 5 percent last year and in the first quarter of this year. Growth came largely from strong exports as the domestic consumption and fixed investment were subdued.

Riksdagens bankfullmäktige reser till USA4.5.2026 11:15:00 EEST | Pressmeddelande

Bankfullmäktige reser till Washington D.C. och New York den 3–8 maj 2026. Under resan träffar bankfullmäktige den högsta ledningen för amerikanska centralbanken Federal Reserve och dess regionala bank i New York samt för Internationella valutafonden (IMF). Under dessa besök informerar sig bankfullmäktige om bland annat framtidsutsikterna för den amerikanska ekonomin och den globala ekonomin, USA:s penning- och finanspolitik samt den senaste utvecklingen inom den finansiella sektorn och det internationella finansiella systemet.

Eduskunnan pankkivaltuusto matkustaa Yhdysvaltoihin4.5.2026 11:15:00 EEST | Tiedote

Pankkivaltuusto matkustaa Washington D.C:hen ja New Yorkiin 3.–8.5.2026. Matkan aikana pankkivaltuusto tapaa Yhdysvaltain keskuspankkijärjestelmän ja sen New Yorkin aluepankin sekä Kansainvälisen valuuttarahaston (IMF) ylintä johtoa. Pankkivaltuusto perehtyy näissä tapaamisissa muun muassa Yhdysvaltain ja globaalin talouden näkymiin, Yhdysvaltain raha- ja finanssipolitiikkaan sekä rahoitussektorin ja kansainvälisen rahoitusjärjestelmän viimeaikaiseen kehitykseen.

In our pressroom you can read all our latest releases, find our press contacts, images, documents and other relevant information about us.

Visit our pressroom