Housing loan maturities have lengthened

27.3.2026 10:00:00 EET | Suomen Pankki | Press release

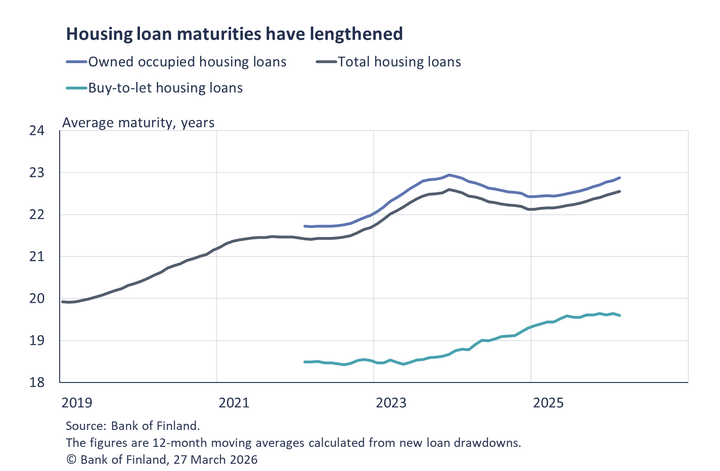

The average maturity of new housing loans has lengthened over the past year. This lengthening has been particularly pronounced in loans for owner-occupied housing. In some housing loans, interest rate resets may also affect the final maturity of the loan.

In February 2026, the average maturity of new drawdowns of loans by households for owner-occupied housing was 23 years and 4 months. The last time when average maturities were this long was in March 2023, before the Consumer Protection Act was amended1. The average maturity of housing loans to Finnish households has lengthened steadily since the beginning of 2025. A year earlier, in February 2025, the average maturity of new drawdowns of owner-occupied housing loans was 11 months shorter. The average maturity has lengthened in particular due to the increase in 25–30-year loans. In owner-occupied housing loans, the most common maturity ranges are 20–25 and 25–30 years. In February 2026, of new drawdowns of owner-occupied housing loans, 20% had a maturity of under 20 years, 41% 20–25 years, 35% 25–30 years and 4% over 30 years. The share of loans with a maturity of over 30 years in new owner-occupied housing loan drawdowns peaked in January 2023 at 16%.

The maturities of buy-to-let housing loans are shorter on average than those of owner-occupied housing loans. In February 2026, the average maturity of buy-to-let mortgages was 19 years and 7 months, about two months longer than a year earlier in February 2025. In February 2026, 49% of new drawdowns of buy-to-let mortgages had a maturity of under 20 years, 36% had 20–25 years and the remaining 15% had 25–30 years.

Interest rate resets may affect the final maturity of a housing loan under certain repayment methods. In a fixed equal payments loan2, the maturity lengthens when the reference rate rises and shortens when the reference rate falls. According to calculations based on the Positive Credit Register, 16% of the euro-denominated stock of owner-occupied housing loans used the fixed equal payments amortisation method at the end of February 2026, while 80% of the loan stock had the annuity repayment method3, 3% had equal instalments4 and the remainder had some other repayment method, such as bullet. In terms of the number of loans, 24% of owner-occupied housing loans used the fixed equal payments method, 71% annuity, 4% equal instalments and 1% some other method at the end of February 2026.

Loans

in February 2026, new drawdowns of housing loans by Finnish households amounted to EUR 1.0 billion, which is EUR 60 million less than in the same period a year earlier. Buy-to-let mortgages accounted for EUR 110 million thereof. The average interest rate on new housing loans declined from January, to stand at 2.81% in February. At the end of February 2026, the housing loan stock totalled EUR 105.6 billion, representing an annual growth of 0.1%. Buy-to-let mortgages accounted for EUR 9.1 billion of the housing loan stock. At the end of February, Finnish households held EUR 17.3 billion of consumer credit and EUR 17.8 billion of other loans.

Drawdowns of new loans5 by Finnish non-financial corporations in February totalled EUR 1.7 billion, whereof loans to housing corporations amounted to EUR 340 million. The average interest rate on new corporate loan drawdowns declined from January to 3.76%. At the end of February, the stock of loans granted to Finnish non-financial corporations stood at EUR 109.1 billion, with housing corporations accounting for EUR 46.0 billion.

Deposits

At the end of February 2026, Finnish households’ aggregate deposit stock totalled EUR 116.3 billion, and the average interest rate on these deposits was 0.79%. Overnight deposits accounted for EUR 70.8 billion and deposits with an agreed maturity for EUR 16.2 billion of the total deposit stock. In February, Finnish households concluded new deposit agreements with an agreed maturity worth EUR 1080 million, at an average interest rate of 2.16%.

For further information, please contact

Pauli Korhonen, tel. +358 9 183 2280, email: pauli.korhonen(at)bof.fi

Markus Aaltonen, tel. +358 9 183 2395, email: markus.aaltonen(at)bof.fi.

The next news release on money and banking statistics will be published at 10:00 on 30 April 2026.

Related statistical data and graphs are also available on the Bank of Finland website: https://www.suomenpankki.fi/en/statistics/.

The statistical data are also available via an API from the Bank of Finland’s open data portal. For details, see https://www.suomenpankki.fi/en/statistics/open-data/?epslanguage=en

---

1 The maximum maturity of new housing loan agreements was limited to 30 years from July 2023 onwards. A lender may not use terms in a housing loan agreement under which the maturity of the loan at the time of granting exceeds 30 years from the drawdown date. However, the lender may deviate from the maximum maturity in 10% of the total volume of housing loans granted in each calendar quarter.

2 In a fixed equal payments loan, the monthly payments always stay the same. When the reference rate value changes, the repayment period is adjusted.

3 In an annuity loan, the repayment period is fixed. The amount of the monthly payment is adjusted when the reference rate value changes.

4 In an equal instalments loan, the instalment amount and repayment period are fixed. The amount of the monthly payment is adjusted when the reference rate value changes.

5 Excluding overdrafts and credit card credit.

Keywords

Links

Bank of Finland

The Bank of Finland is the national monetary authority and central bank of Finland. At the same time, it is also a part of the Eurosystem, which is responsible for monetary policy and other central bank tasks in the euro area and administers use of the world’s second largest currency – the euro.

Alternative languages

Subscribe to releases from Suomen Pankki

Subscribe to all the latest releases from Suomen Pankki by registering your e-mail address below. You can unsubscribe at any time.

Latest releases from Suomen Pankki

Kutsu medialle: Suomen Pankin järjestämä Maksufoorumi 27.5.202621.5.2026 09:00:00 EEST | Kutsu

Tilaisuuden teemat ovat maksamisen ekosysteemin muutos ja maksupetosten torjunta.

Kraftfull finansiell reglering nödvändig för att skydda mot kriser20.5.2026 10:00:00 EEST | Pressmeddelande

Det finansiella systemet i Finland är fortsatt stabilt, fastän internationella konflikter tidvis har skakat finansmarknaden och de stigande marknadsräntorna har fått bostadshandeln att bromsa in. Kraftfulla regler för banker skyddar mot finanskriser och stöder hållbar ekonomisk tillväxt. Man bör inte ge avkall på de finländska bankernas och låntagarnas slagkraftighet. En djupare europeisk kapitalmarknad skulle ge fart åt tillväxten och förstärka Europas strategiska autonomi.

Vahvaa rahoitussääntelyä tarvitaan suojaksi kriiseiltä20.5.2026 10:00:00 EEST | Tiedote

Suomen rahoitusjärjestelmä on pysynyt vakaana, vaikka kansainväliset konfliktit ovat ajoittain ravisuttaneet rahoitusmarkkinoita ja markkinakorkojen nousu on hidastanut asuntokauppaa. Vahva pankkisääntely suojaa finanssikriiseiltä ja tukee kestävää talouskasvua. Suomalaisten pankkien ja lainanottajien iskunkestävyydestä ei tulisi tinkiä. Syvemmät eurooppalaiset pääomamarkkinat vauhdittaisivat kasvua ja vahvistaisivat Euroopan strategista autonomiaa.

Strong financial regulation needed for shielding against crises20.5.2026 10:00:00 EEST | Press release

Finland’s financial system has remained stable, although financial markets have been shaken at times by international conflicts and the housing market has slowed due to the rise in market interest rates. Strong banking regulation provides protection against financial crises and underpins sustainable economic growth. The resilience of Finnish banks and borrowers should not be compromised. Deeper European capital markets would boost growth and strengthen Europe’s strategic autonomy.

Kutsu medialle: Suomen Pankin tiedotustilaisuus 20.5. rahoitusjärjestelmän vakaudesta13.5.2026 13:55:34 EEST | Kutsu

Miten ajankohtaiset kansainväliset konfliktit vaikuttavat talouteen ja rahoitusjärjestelmään? Miten voidaan jatkossakin turvata Suomen pankkisektorin ja lainanottajien riskinkestävyys? Miltä asuntomarkkinoilla näyttää? Mikä olisi yhteisen eurooppalaisen talletussuojan merkitys?

In our pressroom you can read all our latest releases, find our press contacts, images, documents and other relevant information about us.

Visit our pressroom