Economic Forecast 2026–2028: Adrift and Searching for Direction

10.4.2026 12:04:25 EEST | Työn ja talouden tutkimus LABORE | Tiedote

The Finnish economy is returning to modest growth, but its direction remains uncertain. Growth is supported by domestic demand, investment, and private consumption, while international risks, geopolitical tensions, and weak public finances continue to weigh on the outlook. The forecast expects slow growth in the coming years without a recession, but public debt will keep rising and the economic outlook remains subject to exceptionally high uncertainty.

- Growth once again faces international headwinds.

- The growth forecast has been revised downward since autumn, but we do not expect a recession.

- Private consumption and investment are sustaining growth.

- The weak state of public finances is persistent and will not improve over the forecast period.

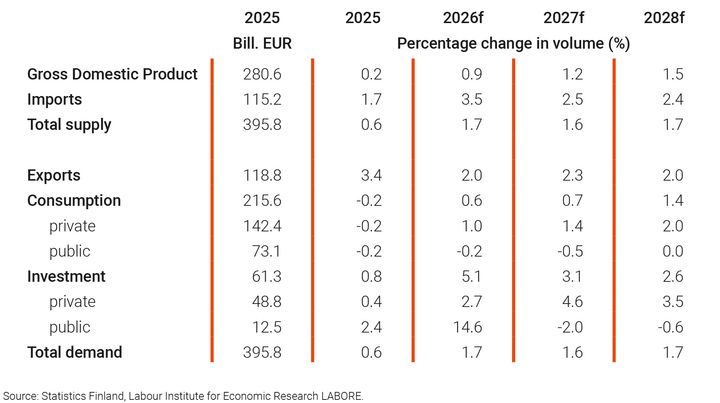

Toward the end of last year, the Finnish economy returned to modest growth, supported by the long-awaited recovery in domestic demand. Private investment and household consumption picked up in the second half of the year, improving growth prospects for early this year. Even so, average economic growth for the year as a whole remained subdued at 0.2 per cent, according to preliminary data. As in 2023 and 2024, external demand was the main driver of growth. The contribution of public demand faded to zero over the course of last year. Given the need for fiscal consolidation, no major change is expected over the forecast horizon. Within private investment, construction showed the first signs of recovery, as the steep downturn of 2023–2024 appeared to have come to an end.

We expect the economy to grow by 0.9 per cent this year. This is 0.5 percentage points lower than in our autumn forecast. Unpredictable policy actions by the United States have sharply increased global uncertainty, weighing on this year's growth outlook despite the more encouraging developments seen toward the end of last year. A further escalation of the war involving Iran into a broader regional conflict would pose an even greater risk to the global economy. A prolonged, multi-country war would push oil prices permanently higher, disrupt supply chains, and increase both prices and interest rates. If these risks were to materialise, growth in Finland and the euro area could stall this year.

Demand and supply

In 2027 and 2028, economic growth is expected to accelerate to 1.2 and 1.5 per cent, respectively. The forecast for next year has been revised downward by 0.3 percentage points because of the prolonged instability in the international environment. Since early 2022, the Finnish economy has been hit by a series of external shocks that have made households and firms increasingly cautious. Russia's war of aggression in Ukraine, now in its fifth year, and the prolonged conflicts in the Middle East have at different times driven up interest rates and unemployment, as well as fuel and electricity prices. Economic decision-making has become more difficult, as reflected for example in the long stagnation of the housing market. In uncertain times, firms and households postpone investment.

At the same time, the current international situation also leaves room for positive surprises. A swift end to the war involving Iran would likely give growth a modest boost by easing uncertainty and lowering market interest rates. Foreign trade would strengthen as demand for Finnish investment goods increased. An end to Russia's war of aggression would bolster household confidence in Finland and improve the economic outlook, especially in Eastern Finland. Although the end dates of these wars remain difficult to predict, the steady stream of negative news in recent years should not obscure the possibility of a more positive outcome.

Outlook for the next few years

So far this year, the global economy has been at the mercy of great power politics. The rapidly shifting operating environment has heightened uncertainty about the world trade outlook. Even so, we expect the major economies to continue growing over the forecast period. The United States benefits from strong domestic demand and investments in artificial intelligence. The euro area is suffering from disruptions in oil and natural gas supplies, but the impact on growth is likely to remain moderate. China has again shown its flexibility by redirecting exports to other markets in response to U.S. trade policies. However, the conflict in the Middle East is creating risks to the availability of oil imports from the Middle East, which poses a downside risk to Chinese growth.

According to data for February, the unemployment rate stood at 10.5 per cent. Unemployment has risen in recent years because more people have become unemployed both from employment and, in particular, from outside the labour force. This reflects the weak state of the economy, cuts in the public sector, and government measures that have increased labour supply. At the same time, the number of employed people has declined but remains at a reasonably solid level. The unemployment figures therefore paint a somewhat darker cyclical picture than the broader reality. We expect unemployment to start falling during this year and to remain at 9.7 per cent over the forecast period. We also expect labour productivity to improve as the cyclical recovery gathers pace. Output per hour worked is set to rise faster than before, supporting overall economic growth.

Inflation slowed to 0.2 per cent last year as energy prices and interest rates declined. Measured by the harmonised index of consumer prices, inflation was 1.8 per cent, as this measure excludes owner-occupied housing and interest costs. Inflation forecasting is currently subject to exceptional uncertainty because of fluctuations in oil prices. We expect national inflation to rise to 1.9 per cent this year, driven above all by higher energy prices. We do not anticipate a repeat of the inflation spike seen in 2022-2023. Instead, inflation is expected to remain close to, but slightly above, 2 per cent in 2027 and 2028.

Investments will grow above all because of fighter aircraft purchases recorded this year and next. We also expect construction investment to recover gradually. Residential construction is likely close to its trough, while data-centre-related building projects have expanded rapidly. Investments in R&D will also increase over the forecast period, supported by additional public funding and a tax incentive targeted at the private sector. We forecast investment growth of 5.1 per cent this year, 3.1 per cent in 2026, and 2.6 per cent in 2027.

Finland's public finances are unlikely to improve in the near term. Deficits and the pace of debt accumulation will remain high for several more years. Spending pressures are being driven by healthcare and long-term care costs related to population ageing, pensions, higher interest expenditure, and the growing need for defence investment arising from the security situation. At the same time, economic growth is too weak to strengthen the revenue base sufficiently. This year, the ratio of public debt to GDP will exceed 90 per cent, placing Finland above the EU average.

Avainsanat

Yhteyshenkilöt

Juho KoistinenennustepäällikköMakrotalous, ennusteet ja toimialatalous

Puh:040 940 2833juho.koistinen@labore.fiLiitteet

Linkit

Labore eli Työn ja talouden tutkimus LABORE (ent. Palkansaajien tutkimuslaitos) on vuonna 1971 perustettu itsenäinen tutkimuslaitos, jossa keskitytään yhteiskunnallisesti merkittävään ja tieteen kansainväliset laatukriteerit täyttävään soveltavaan taloustieteelliseen tutkimukseen. Tutkimuksen painopistealueisiin kuuluvat työn taloustiede, julkistaloustiede sekä makrotaloustiede ja toimialan taloustiede. Lisäksi teemme suhdanne-ennusteita ja toimialakatsauksia sekä julkaisemme Talous & Yhteiskunta -lehteä ja podcasteja.

Vahvuuksiamme ovat tutkijoiden korkea tieteellinen osaaminen sekä tiivis yhteistyö kotimaisten ja ulkomaisten yliopistojen ja tutkimuslaitosten kanssa. Tutkijoillamme on tärkeä asiantuntijarooli eri yhteyksissä ja he osallistuvat aktiivisesti yhteiskunnalliseen keskusteluun.

Tilaa tiedotteet sähköpostiisi

Haluatko tietää asioista ensimmäisten joukossa? Kun tilaat tiedotteemme, saat ne sähköpostiisi välittömästi julkaisuhetkellä. Tilauksen voit halutessasi perua milloin tahansa.

Lue lisää julkaisijalta Työn ja talouden tutkimus LABORE

Helleaallot, pandemiat ja hintashokit paljastavat sosiaaliturvan aukot1.7.2026 08:20:30 EEST | Tiedote

Sään ääri-ilmiöt, pandemiat, inflaatio ja velkakriisit näyttävät erilaisilta kriiseiltä, mutta kotitalouksien arjessa ne voivat johtaa samaan lopputulokseen: työnteko vaikeutuu, ruoan ja energian hinta nousee ja toimeentulo joutuu äkillisesti koetukselle. Vastapainon tuoreessa Globaali sosiaalipolitiikka -teoksessa julkaistu luku "Talousshokit ja -kriisit hyvinvoinnin haasteena" tarkastelee, miten matalan ja keskitulotason maat ovat vastanneet talousshokkeihin sosiaali- ja talouspolitiikan keinoin. Laboren johtava tutkija Milla Nyyssölän yhdessä tutkijaryhmän kanssa kirjoittamassa luvussa korostetaan, että kriisinkestävyys rakennetaan ennen kriisiä: toimivat tukiohjelmat, maksujärjestelmät, veropohja ja julkiset instituutiot ratkaisevat, kuinka nopeasti toimeentuloa suojaava tuki saavuttaa tarpeessa olevat.

Tutkimus: Alustatyöntekijät eivät ole yhtenäinen ryhmä Suomessa30.6.2026 11:28:18 EEST | Tiedote

Uusi tutkimus tuo kansallisesti edustavan kysely- ja rekisteriaineiston avulla tutkimustietoa siitä, ketkä tekevät alustatyötä Suomessa ja miten alustatyö kytkeytyy muuhun ansiotyöhön. Tulosten mukaan alustatyön tekeminen on voimakkaasti yhteydessä ulkomaalaistaustaan, mutta paikan päällä ja verkossa tehtävän alustatyön tekijäprofiilit poikkeavat selvästi toisistaan. Paikan päällä tehtävä alustatyö liittyy erityisesti ulkomaalaistaustaan ja kaupunkiasumiseen, kun taas verkossa tehtävä alustatyö on yhteydessä sekä korkeampaan koulutustasoon että matalampaan tulotasoon. Tutkimus osoittaa myös, että alustatyö kytkeytyy muuhun ansiotyöhön eri tavoin kuin perinteinen usean työn tekeminen.

Tarveperusteinen rahoitus ja arvioinnin haasteet23.6.2026 07:00:00 EEST | Blogi

Tarveperusteisen rahoituksen tavoitteista vallitsee Suomessa laaja yksimielisyys, mutta järjestelmän vaikuttavuuden arviointi on vaikeaa ilman tarkkaa tietoa rahojen lopullisesta kohdentumisesta. Jos emme tiedä, kuinka paljon rahoitusta yksittäiset koulut saavat ja mihin sitä käytetään, emme myöskään voi luotettavasti arvioida, kaventaako rahoitus koulutuksellisia eroja.

Tekoälyn tuottavuus- ja työllisyysvaikutukset – mitä on luvassa lähivuosina?18.6.2026 06:45:00 EEST | Blogi

Tekoälyn vaikutukset työpaikkoihin ja tuottavuuteen eivät todennäköisesti näy yhdessä yössä. Taloustieteellinen tutkimus viittaa siihen, että suurimmat vaikutukset syntyvät viiveellä, kun yritykset uudistavat toimintatapojaan, tuotteitaan ja liiketoimintamallejaan uuden teknologian ympärille. Suomen kannalta ratkaisevaa on, onnistuuko talous luomaan ympäristön, jossa osaaminen, innovaatiot ja kasvuyritykset pääsevät skaalautumaan.

Julkisen talouden sopeutus ei ole yksinkertainen valinta leikkausten ja veronkorotusten välillä16.6.2026 06:45:00 EEST | Tiedote

Suomen julkisen talouden sopeutuksessa on kyse paitsi menoleikkausten ja veronkorotusten välisestä valinnasta, myös siitä, mihin julkiset resurssit kohdistetaan. Mika Malirannan tuore Kansantaloudellisessa aikakauskirjassa julkaistu pääkirjoitus korostaa, että aiemmat vahvat johtopäätökset menoleikkausten paremmuudesta ovat selvästi epävarmemmalla pohjalla kuin on usein ajateltu. Talouspolitiikassa jokaisella eurolla on vaihtoehtoiskustannus: esimerkiksi perintöveron poistoa ei voi arvioida irrallaan siitä, mitä vaihtoehtoisella verotulon käytöllä tai menetyksen kattamisella saavutettaisiin.

Uutishuoneessa voit lukea tiedotteitamme ja muuta julkaisemaamme materiaalia. Löydät sieltä niin yhteyshenkilöidemme tiedot kuin vapaasti julkaistavissa olevia kuvia ja videoita. Uutishuoneessa voit nähdä myös sosiaalisen median sisältöjä. Kaikki tiedotepalvelussa julkaistu materiaali on vapaasti median käytettävissä.

Tutustu uutishuoneeseemme