Drawdowns of new housing loans in July lower than usual

31.8.2023 10:00:00 EEST | Suomen Pankki | Press release

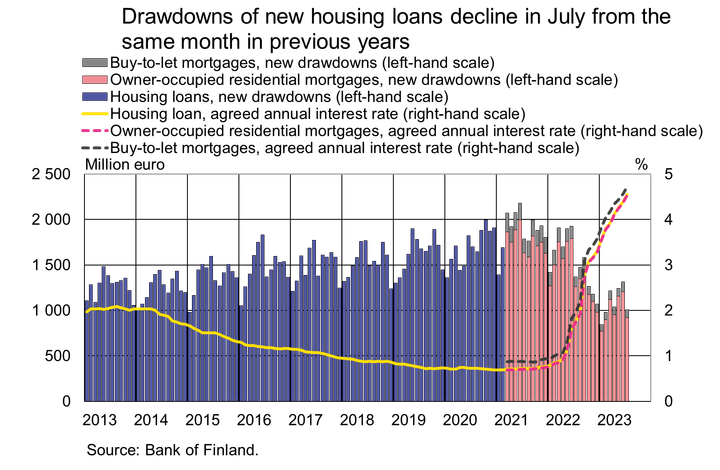

Drawdowns of new housing loans in July 2023 totalled EUR 1.0 bn, a decline of 27% on the corresponding month last year. The last time housing loan drawdowns were this low in July was in 2002. In July 2023, the average interest rate on new housing loans stood at 4.55%. The average interest rate on new housing loans has not been higher than this since November 2008.

Drawdowns of new housing loans in July 2023 totalled EUR 1.0 bn, a decline of 27% on the corresponding month last year.1 The last time housing loan drawdowns were this low in July was in 2002. Buy-to-let mortgages accounted for EUR 86 million of the new housing loans in July, down 22% from the same period a year ago.

In July 2023, the average interest rate on new housing loans stood at 4.55%. The average interest rate on new housing loans has increased markedly (by a percentage point) from the beginning of the year. The average interest rate on new housing loans has not been higher than this since November 2008. Average interest rates on both owner-occupied and buy-to-let mortgages have risen. The average interest rate on new owner-occupied residential mortgages stood at 4.53% in July 2023. At the same time, the interest rate on new buy-to-let mortgages was higher, at 4.72%.

In July, the average repayment period of housing loans was 22 years and 7 months. The proportion of loans with a repayment period of over 30 years declined to 7% of new drawdowns. In 2023 up to July, the proportion ranged from 13% to 15%. As of July 2023, households are required to repay new housing loans in a maximum of 30 years.2 However, banks may deviate from the maximum maturity in 10% of their lending.

In July 2023, 95% of new drawdowns of housing loans were linked to Euribor rates, with the remaining 5% being linked to other reference rates.3 The 12-month Euribor was used as the reference rate in 51% of new Euribor-linked housing loans, as opposed to 93% in July last year. Following the rise in the level of interest rates, the shorter 3- or 6-month Euribor rates have been used increasingly as reference rates for housing loans.

Loans

At the end of July 2023, the housing loans stock totalled EUR 106.9 billion, and its year-on-year growth amounted to -1.6%. Buy-to-let mortgages accounted for EUR 8.6 billion of the housing loan stock. At the end of July, the household loan stock included EUR 17.1 billion of consumer credit and EUR 17.7 billion of other loans.

Drawdowns of new loans4 by Finnish non-financial corporations amounted to EUR 1.6 billion, with loans to housing corporations accounting for EUR 350 million. The average interest on new corporate loan drawdowns rose from June to stand at 5.56%. At the end of July, the stock of loans granted to Finnish non-financial corporations stood at EUR 105.3 billion, whereof loans to housing corporations accounted for EUR 43.3 billion.

Deposits

At the end of July 2023, the stock of Finnish households’ deposits totalled EUR 109.9 billion, and the average interest rate on these deposits was 0.78%. Overnight deposits accounted for EUR 80.5 billion and deposits with an agreed maturity for EUR 7.4 billion of the total deposit stock. In July, Finnish households made new agreements on deposits with an agreed maturity in the amount of EUR 400 million. In July, the average interest rate on deposits with an agreed maturity was 2.91%.

For further information, please contact:

Usva Topo, tel. +358 9 183 2056, email: usva.topo(at)bof.fi.

Markus Aaltonen, tel. +358 9 183 2395, email: markus.aaltonen(at)bof.fi.

The next news release on money and banking statistics will be published at 10:00 on on 28 September 2023.

Related statistical data and graphs are also available on the Bank of Finland website: shttps://www.suomenpankki.fi/en/Statistics/saving-and-investing/.

[1] Average drawdowns of new housing loans in the month of July in 2012–2022 amounted to EUR 1.5 billion.

[2] Further information on the Government website: https://valtioneuvosto.fi/en/-//10623/limitations-on-loans-to-households-and-housing-companies-to-be-introduced-at-the-beginning-of-july

[3] Banks’ own reference rates, fixed interest rates or other interest rates.

[4] Excl. overdrafts and credit card credit.

The Bank of Finland is the national monetary authority and central bank of Finland. At the same time, it is also a part of the Eurosystem, which is responsible for monetary policy and other central bank tasks in the euro area and administers use of the world’s second largest currency – the euro.

Subscribe to releases from Suomen Pankki

Subscribe to all the latest releases from Suomen Pankki by registering your e-mail address below. You can unsubscribe at any time.

Latest releases from Suomen Pankki

Kutsu medialle: Suomen Pankin tiedotustilaisuus 12.6.2026 Suomen talouden näkymistä4.6.2026 10:51:25 EEST | Kutsu

Piristyykö talouskasvu? Kuinka vakavasti Lähi-idän konflikti hämärtää talouden näkymiä? Onko inflaation nopeutuminen tilapäinen ilmiö? Millä tavalla talouskasvun kiihtyminen vaikuttaisi työvoimaan kysyntään ja työttömyyteen?

Omedelbara betalningar blev vanligare 20254.6.2026 10:00:00 EEST | Pressmeddelande

Sekundsnabba betalningar, dvs. omedelbara betalningar blev vanligare 2025. Sedan januari 2025 har bankerna i euroområdet varit skyldiga att ta emot och sedan oktober 2025 att skicka kundernas omedelbara betalningar. De omedelbara betalningarnas andel av samtliga kontoöverföringar är fortfarande liten, även om omedelbara betalningar görs mer än tidigare.

Pikamaksamisen osuus tilisiirroista kasvoi vuonna 20254.6.2026 10:00:00 EEST | Tiedote

Vain sekunneissa tapahtuvat maksut eli pikamaksut yleistyivät vuonna 2025. Euroalueen pankkien on pitänyt tammikuusta 2025 lähtien vastaanottaa ja lokakuusta lähtien lähettää asiakkaiden pikamaksuja. Pikamaksujen euromääräinen osuus kaikista tilisiirroista on jäänyt vielä pieneksi, vaikka pikamaksuja tehdään aiempaa enemmän.

Instant payments became more common in 20254.6.2026 10:00:00 EEST | Press release

Payments completed in just seconds, i.e. instant payments, became more common in 2025. Since January 2025, euro area banks have been required to receive instant payments, and since October they have also been required to send customers’ instant payments. Although the number of instant payments has increased, their share of the total value of credit transfers remains small.

Fordonslån beviljades sparsamt under det första kvartalet 20263.6.2026 10:00:00 EEST | Pressmeddelande

Framför allt övriga finansinstitut beviljade klart mindre nya fordonslån jämfört med ett år tidigare. Genomsnittsräntan på fordonslån sjönk något från året innan.

In our pressroom you can read all our latest releases, find our press contacts, images, documents and other relevant information about us.

Visit our pressroom